Finance of America Mortgage

Finance of America Mortgage

Singles need to be better prepared than couples to buy a home

___

Published Date 2/12/2018

Realtor Report

Singles need to be better prepared than couples to buy a home

Homeownership remains a goal for many couples. But what about the singles who dream of it as well? According to Zillow, saving for a down payment is no walk in the park for future home buying couples, but an even more challenging prospect to singles, for whom it may take up to 11 years to save up for a down payment for a typical U.S. home (even longer in pricey markets). This is more than twice the time it takes a married or partnered couple.

With the typical single buyer being able to afford a home up to $176,100, that figure is less than the national median home value. That means that fewer than half (45 percent) of all U.S. homes are affordable for him or her. Couples, by contrast, could afford 82 percent of all homes.

Banks are not allowed to discriminate based on marital status, but tighter lending standards can potentially pose a challenge to single buyers because they only have their own income to qualify for a loan. So how can the average single person make home ownership a reality?

According to a Money Magazine article on the topic, there are a few questions singles should ask themselves to make this process more manageable. First, they should scrutinize their finances carefully and evaluate whether buying a home is even feasible, especially since they won't have help from a partner to pay the bills or make a mortgage payment. Taking steps like reviewing their credit reports and cleaning up any mistakes as well as paying down debt (including student loans) can go a long way to being prepared to take the monumental step of applying for a mortgage.

He or she should also consider the recurring expenses associated with homeownership beyond the purchase price and mortgage closing costs. This may include association fees, property taxes, utilities and lawn care, as well as insurance. Even for couples, these things are often not considered seriously enough when taking on a mortgage, finding them giving up a lot of the things they used to love doing and enjoying because they have suddenly become house poor. This means singles should probably have an even bigger savings account than couples, according to many sources, since unexpected expenses will rely on just one income and the retention of one job. A simple case of bathroom mold can soak a new condo owner to the tune of $10,000 if the place needs to be gutted and remodeled.

If a single (especially a single parent) finds it difficult to come up with the entire down payment or qualify for a conventional mortgage, there may be income-restricted loan programs that offer down payment assistance in many states and locales.

Home ownership is still within reach for singles, but it's important to note that they have a somewhat steeper hill to climb to get the keys to that shiny new front door.

Source: TBWSThis Week's Mortgage Rate Summary

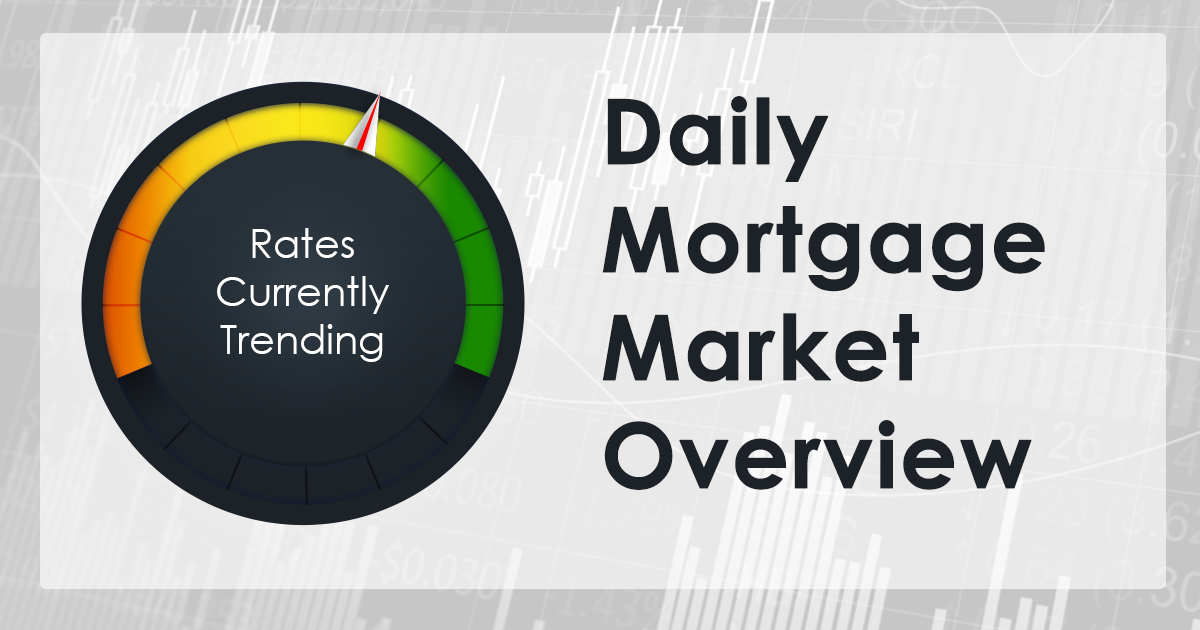

How Rates Move:

Conventional and Government (FHA and VA) lenders set their rates based on the pricing of Mortgage-Backed Securities (MBS) which are traded in real time, all day in the bond market. This means rates or loan fees (mortgage pricing) moves throughout the day, being affected by a variety of economic or political events. When MBS pricing goes up, mortgage rates or pricing generally goes down. When they fall, mortgage pricing goes up.

Rates Currently Trending: Neutral

Mortgage rates are trending sideways to slightly lower so far today. Last week the MBS market worsened by -11bps. This may've moved mortgage rates slightly higher last week. Mortgage rate volatility was very high last week.

This Week's Rate Forecast: Neutral

Three Things: These are the three things that have the greatest ability to move mortgage rates this week: 1) Domestic, 2) Across the Pond and 3 ) Geopolitical.

1) Domestic: Inflation Watch. The biggest event of the week is the CPI report on Wednesday. It is unusual because it is released this week before PPI which is released the next day. It is usually the other way around. This report is expected to show inflation at above 2%. The higher it is, the worse it will be for mortgage rates. We also have Retail Sales that same day which will be important to watch. Also, with bonds focusing on increased deficits (which are always inflationary), Monday's Treasury Budget will get a lot of attention as it will be the first budget that has the tax cut in it.

2) Across the Pond: Besides the Olympics, there's plenty going on overseas. In the order of the largest economies (besides the U.S.): China - Chinese New Year, Japan - GDP, Germany - GDP, CPI, Great Britain - PPI, CPI and Retail Sales, Eurozone - GDP.

3) Geopolitical: The bond market is hedging towards global central banks tightening in the near future along with tapering bond purchases, we also have our own infrastructure and budget/deficit concerns with the 2019 budget proposal out of the White House.

This Week's Potential Volatility: High

Mortgage rates will pay close attention to the CPI report on Wednesday. Look for continued volatility, particularly if the stock market continues its wild swings.

Bottom Line:

If you are looking for the risks and benefits of locking your interest rate in today or floating your loan rate, contact your mortgage professional to discuss it with them.

Source: TBWSAll information furnished has been forwarded to you and is provided by thetbwsgroup only for informational purposes. Forecasting shall be considered as events which may be expected but not guaranteed. Neither the forwarding party and/or company nor thetbwsgroup assume any responsibility to any person who relies on information or forecasting contained in this report and disclaims all liability in respect to decisions or actions, or lack thereof based on any or all of the contents of this report.

©2015 Finance of America Mortgage LLC | Equal Housing Lender | NMLS 1071 Complaints@financeofamerica.com

Thomas Werbeckes

Mortgage Advisor

NMLS: 1543335

Finance of America Mortgage

6900 S McCarran Blvd #2020, Reno NV

Company NMLS: 1071

Office: 775-332-6629

Cell: 775-742-9128

Email: twerbeckes@financeofamerica.com

Web: http://www.financeofamerica.com/locations/branch-profile?id=c33827bb-71f8-6483-85d2-ff00007a9d7f

Thomas Werbeckes

___

Mortgage Advisor

NMLS: 1543335

Cell: 775-742-9128

Last articles

___

Load more